BANKING

How Banks Work

Knowing how banks work helps you understand where your money goes, how interest builds, and why fees exist.

Banks are financial institutions that hold your money, help you make payments, and provide loans. They make money by charging interest on loans and using deposited funds for investments, while paying you interest on your savings. Your money is safe at banks because deposits are insured up to $250,000 by the FDIC (for banks) or NCUA (for credit unions).

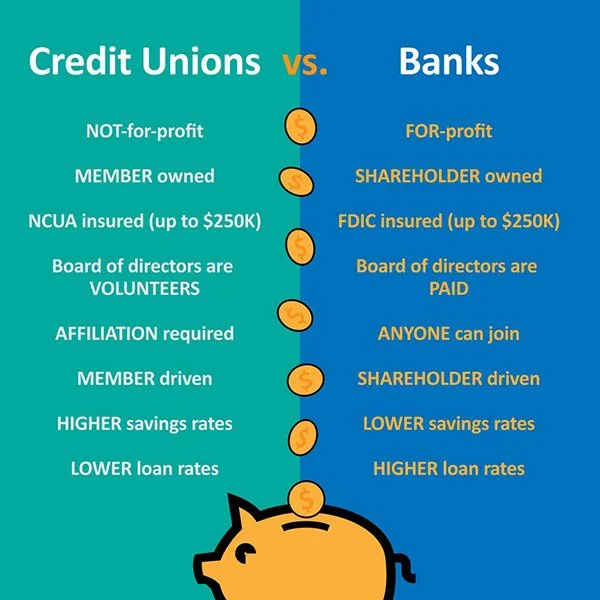

Credit Unions vs Banks

Credit Unions: These are non-profit, member-owned cooperatives. They are known for offering better interest rates, having lower fees, and focusing on serving the community as well as their members.

Example: Desert Financial Credit Union

Banks: They are for-profit institutions owned by shareholders. They offer more branches/locations, bigger technology platforms, sometimes more advanced financial products, and broader services.

Example: Wells Fargo

How to Choose a Bank

When picking a bank or credit union, consider:

Fees: Monthly maintenance fees, ATM withdrawal fees, and overdraft fees can add up. Try to avoid accounts that charge unnecessary fees.

Minimum balances: Some accounts require you to keep a certain amount in your account to earn interest or avoid fees.

Interest rates: Higher rates on savings accounts or CDs means your money grows faster.

Accessibility: Are there branches or ATMs nearby? Does the bank have a good mobile app? These will help determine convenience.

Customer service: Friendly, responsive service can save time if issues arise

Pro Tip: Many banks and credit unions offer student-friendly checking and savings accounts. These usually have no monthly fees and low minimum balances.

Within the Bank

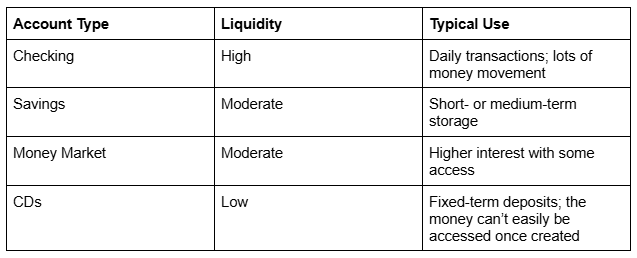

Checking Accounts

A checking account is a type of bank account designed for everyday money management. This includes things like food delivery, Netflix, and rent.

Key features include:

Easy access: Funds can be withdrawn or spent at any time using debit cards, ATMs, or digital payments such as Apple Pay. They are very liquid

Fees to watch: Monthly maintenance, overdraft charges, ATM withdrawal, and out-of-network fees

Usually comes with a debit card, checks, and online/mobile banking

Usually does not have interest, but if it does, it’s very low (<0.1%)

Savings accounts

Savings accounts are designed to hold money for the medium or long term while earning interest. They are considered low-risk because the principal is typically protected.

Types of Savings Accounts:

Traditional Savings Accounts: Standard accounts with modest interest

High-Yield Savings Accounts: Accounts that offer higher rates, often online-only, while maintaining deposit insurance

Student Savings Accounts: Accounts tailored to students with lower minimum balances or fees

Money Market Accounts: Accounts that sometimes combine features of checking and savings, often with higher interest and limited transaction access

Definition of Interest: Interest is money earned on deposits over time. If you are giving money to be borrowed, you are the one receiving the interest. This can be simple (on the initial deposit) or compound (on the deposit PLUS accumulated interest).

Example: If you deposit $100 in an account with 5% annual interest:

Simple interest = $5 per year

Compound interest = $5.13 after one year if interest compounds monthly

Certificates of Deposit (CDs)

CDs are accounts where funds are deposited for a fixed term, often earning a higher interest rate than standard savings accounts.

Early withdrawals may result in penalties

Longer terms can result in higher interest rates

You can choose both the amount and duration of a CD

When the term ends, many banks allow the CD to automatically roll over (reinvest) into a new CD of the same or different duration. This is called a CD rollover.

Banks and credit unions will provide you with a list of different durations and rates of interest

Educational example:

Imagine you have $200 in a checking account that you don’t plan to use for a while. You could open a CD for 6 months. If the CD offers 4% interest, the $200 would earn interest over that period, and the total balance at the end of 6 months would include the original $200 plus the earned interest.

Liquidity

Liquidity is the ease with which money can be accessed without penalties.

Observations for Students

Different account types demonstrate trade-offs between liquidity and interest.

Interest rates, fees, and account structures vary by financial institution.

Comparing account features can help understand how money is stored and accessed.

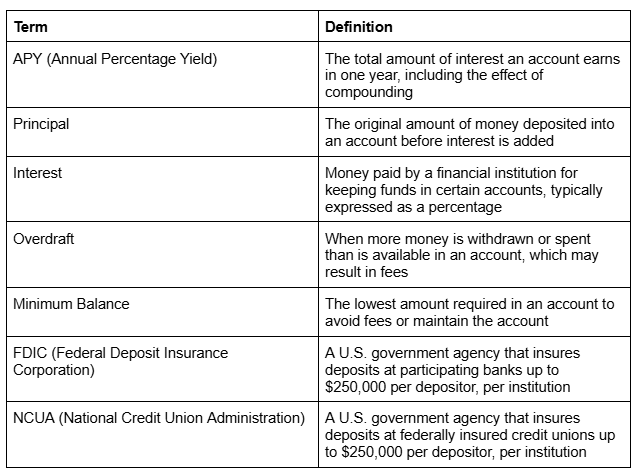

Banking Terms Glossary

Here are some additional helpful terms to know:

sources

https://www.imf.org/external/pubs/ft/fandd/2012/03/basics.htm

https://www.nerdwallet.com/banking/learn/credit-unions-vs-banks

Here is a chart that shares more of the differences!