student loans

Student loans overview

Paying for college can be expensive, and many students consider student loans to help cover costs. This guide is designed to provide educational information so you understand what student loans are, how they work, and what factors to consider.

What are student loans?

Student loans are funds borrowed to pay for education-related expenses such as tuition, fees, housing, and books. Unlike grants or scholarships, loans must be repaid, often with interest.

You can think of it this way too: Loans are a type of debt, and the total amount owed depends on how much you borrow, interest rates, and the repayment schedule.

Types of Student Loans:

1. Federal Student Loans

Funded by the U.S. Department of Education, federal loans often have lower interest rates, structured repayment options, and protections for borrowers.

Common Types:

Direct Subsidized Loans:

Need-based; the government pays interest while you’re in school

Interest does not accrue while enrolled at least half-time

Direct Unsubsidized Loans:

Available to all students; interest accrues immediately

Borrowers are responsible for all interest

Direct PLUS Loans:

For graduate students or parents of undergraduates.

Requires a credit check.

Higher interest rates than other federal loans.

Direct Consolidation Loans:

Allows a borrower to combine two or more federal student loans into a single loan.

Combines multiple payments into one monthly payment, making repayment easier to manage.

Interest rate is a weighted average of the original loans’ rates, rounded up to the nearest 1/8 of a percent

Can simplify repayment, but may affect certain benefits (like some loan forgiveness timelines)

Federal student loans have several key features that affect how they work:

Fixed Interest Rates

Federal loans have interest rates that do not change over the life of the loan. This means your interest rate stays the same whether you graduate in 4 years or take longer to repay

Example: If you borrow $10,000 at a 5% fixed interest rate, the rate remains 5% for the entire repayment period

Various Repayment Plans

Federal loans offer multiple options to pay back your loan:

Standard Repayment Plan: Fixed monthly payments, usually over 10 years

Graduated Repayment Plan: Payments start smaller and increase over time

Income-Driven Repayment Plans: Payments are calculated based on your income and family size; can change as your income changes

These plans provide flexibility, allowing borrowers to select a repayment schedule that aligns with their circumstances

Grace Period After Leaving School

Most federal loans include a 6-month grace period after you graduate, leave school, or drop below half-time enrollment

During this period, you generally do not have to make payments, giving you time to prepare for repayment

Example: If you graduate in May, your first payment would usually be due in November

These features are designed to make federal loans more predictable and flexible for students. Fixed interest rates provide stability, multiple repayment plans offer options to manage monthly payments, and the grace period allows time to transition from school to repayment.

2. Private Student Loans

Private student loans are offered by banks, credit unions, or other financial institutions rather than the federal government.

Credit-based Approval:

Most private loans require a credit check

A co-signer may be needed if the borrower does not meet credit requirements

Variable or Fixed Interest Rates:

Interest rates are determined by the lender and can be fixed or variable

Rates may be higher than federal loans depending on credit history

Repayment Terms Set by the Lender:

Payment schedules, grace periods, and options for changing payments vary

Repayment may begin immediately after leaving school or dropping below half-time

Fewer Protections:

Private loans may not include deferment, forbearance, or loan forgiveness programs

Borrowers are responsible for staying informed about the loan’s rules and terms

Private loans are designed for educational funding but operate differently from federal loans. Understanding their terms, interest rates, and repayment requirements is important for staying informed as a borrower.

How Interest Works

Interest is the cost of borrowing money. Understanding interest accrual can help you see how borrowing more or delaying repayment can affect the total amount owed over time. Different types of loans handle interest differently:

Subsidized Federal Loans: The government pays interest while you’re in school, so your loan balance doesn’t grow.

Unsubsidized Federal Loans: Interest accrues while in school. If unpaid, it may be added to the loan principal, increasing the total amount owed.

Private Loans: Interest accrual varies; it may start immediately and be added to the balance if unpaid.

Repayment Overview

Repayment refers to paying back the loan after leaving school or dropping below half-time enrollment.

Federal Loans:

Grace Period: Usually 6 months after graduation before repayment begins

Repayment Plans:

Standard: Fixed monthly payments over ~10 years

Graduated: Payments start lower and increase over time

Income-Driven: Monthly payments based on income and family size

Private Loans:

Repayment terms vary by lender

Often begin immediately after leaving school

Fewer options for adjusting payments

Repayment really depends on the loan type and the terms outlined in the loan agreement. You can contact your loan servicer for detailed information about repayment options.

Loan Forgiveness & Hardship Options

Certain federal programs provide options for reducing or pausing payments under specific circumstances:

Public Service Loan Forgiveness (PSLF): Available to borrowers working full-time in qualifying public service jobs

Deferment: Temporary pause in payments under approved situations (interest may or may not accrue depending on the loan)

Examples: returning to school at least half-time, serving in the military, enrolling in certain vocational training programs, economic hardship

Forbearance: Temporary reduction or pause in payments, usually with interest continuing to accrue

Examples: temporary unemployment, medical issues or illness, economic hardship, natural disasters or other emergency situations

Eligibility for these programs depends on the loan type and specific requirements.

Should You Apply for Student Loans?

While scholarships, grants, and personal savings are usually the best ways to pay for college, sometimes borrowing is necessary—and that’s okay. Your education is important, but so is understanding how student loans work and how they may affect your finances. If you do need to borrow, federal student loans often provide more protections and benefits than private loans. Here are some key points to keep in mind:

The interest rate on student loans is fixed and usually lower than private student loans

You don't need a credit check or a cosigner to get most federal student loans

You don't have to begin repaying your federal student loans until after you leave college or drop below half-time

Depending on your financial situation, the government pays the interest on some loan types while you are still in school and during some periods after school

Federal student loans offer flexible repayment plans and options to postpone loan payments if you are having trouble making payments

If you work in certain jobs, you may be eligible to have a portion of your federal student loans forgiven if you meet certain conditions

Educational Tips for Staying Organized

You can manage your loans responsibly by staying informed:

Track all loans using the Federal Student Aid portal

Keep copies of all loan documents

Understand the terms, interest rates, and repayment schedules

Monitor accrued interest

Stay in contact with your loan servicer for updates or questions

Your College’s Financial Aid Office – they usually provide resources, workshops, and general guidance

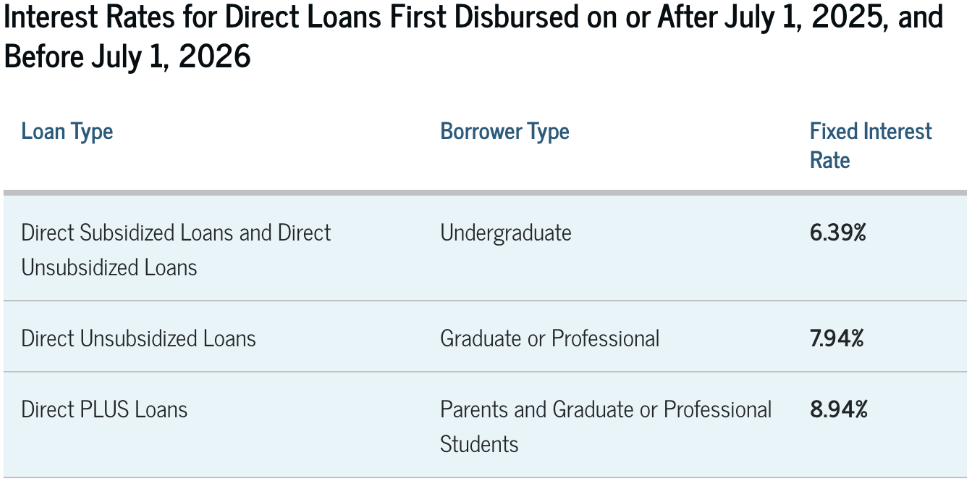

Interest Rates (2025 - 2026)

Helpful Tools & Resources

Managing student loans can feel overwhelming, but there are several trusted resources to help you stay informed and organized:

Federal Student Aid (studentaid.gov)

Track all your federal student loans in one place.

View balances, servicers, and repayment plans.

Apply for deferment, forbearance, or loan consolidation.

ASU Financial Aid Office

General information on loans, grants, and scholarships.

Workshops and guidance on understanding loan responsibilities.

Consumer Financial Protection Bureau – Student Loans

Educational guides on student loans, repayment options, and borrower rights.

Tools to compare loan types and understand interest and payments.

Loan Calculators

Check out our debt calculator on our website: https://www.collegemoneymind.com/debt-calculator

Use other online calculators to estimate monthly payments and total interest

Remember, these resources are intended for educational purposes only. They provide information to help you understand and manage your loans. Everyone’s financial situation is different, so we cannot offer personalized financial advice.

Sources

Disclaimer: This information is provided as an educational resource. College Money Mind does not receive compensation for recommendations and encourages students to research options before making financial decisions.